A Parent Company Comfort Letter provides a formal assurance to lenders regarding a subsidiary's financial obligations. While not a legally binding guarantee, it demonstrates the parent's commitment to support the subsidiary's creditworthiness and debt repayment. This document is essential for securing favorable loan terms and building lender confidence. To assist your documentation process, below are some ready to use templates.

Image cover: A Guide to Parent Company Comfort Letters: Templates and Samples for Subsidiary Financing

Letter Samples List

- Parent Company Comfort Letter for Subsidiary Credit Facility

- Letter of Comfort for Subsidiary Term Loan Agreement

- Standard Keepwell Letter for Subsidiary Borrowing

- Letter of Support for Subsidiary Working Capital Financing

- Parent Company Awareness Letter for Subsidiary Overdraft Facility

- Letter of Comfort for Subsidiary Revolving Credit Line

- Financial Support Letter for Subsidiary Trade Finance Facility

- Parent Company Comfort Letter for Subsidiary Project Financing

- Letter of Sponsorship for Subsidiary Syndicated Loan Facility

- Binding Comfort Letter for Subsidiary Bridge Financing

- Non-Binding Comfort Letter for Subsidiary Debt Obligation

- Parent Company Letter of Assurance for Subsidiary Corporate Borrowing

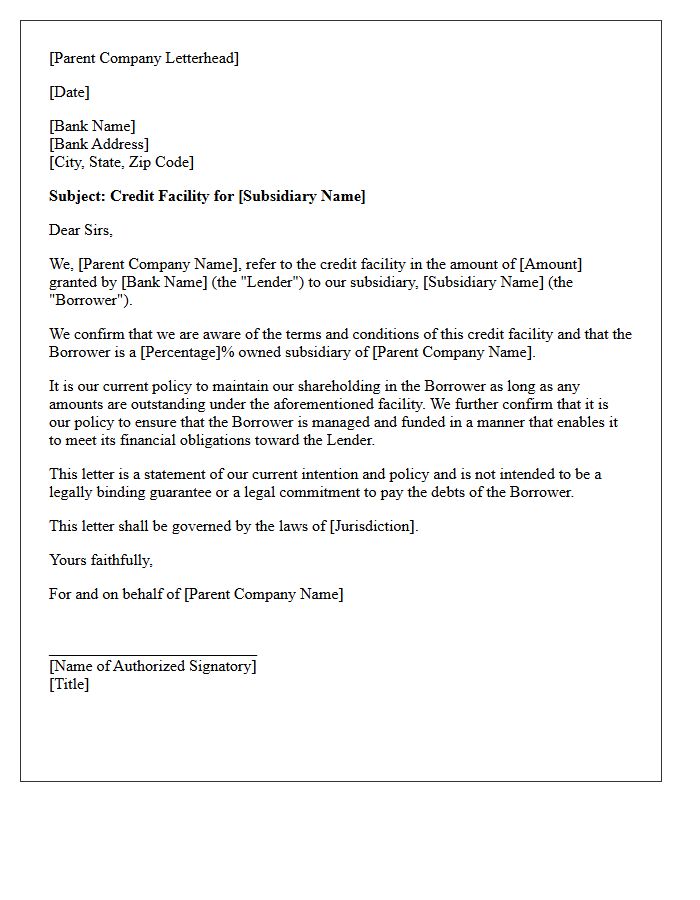

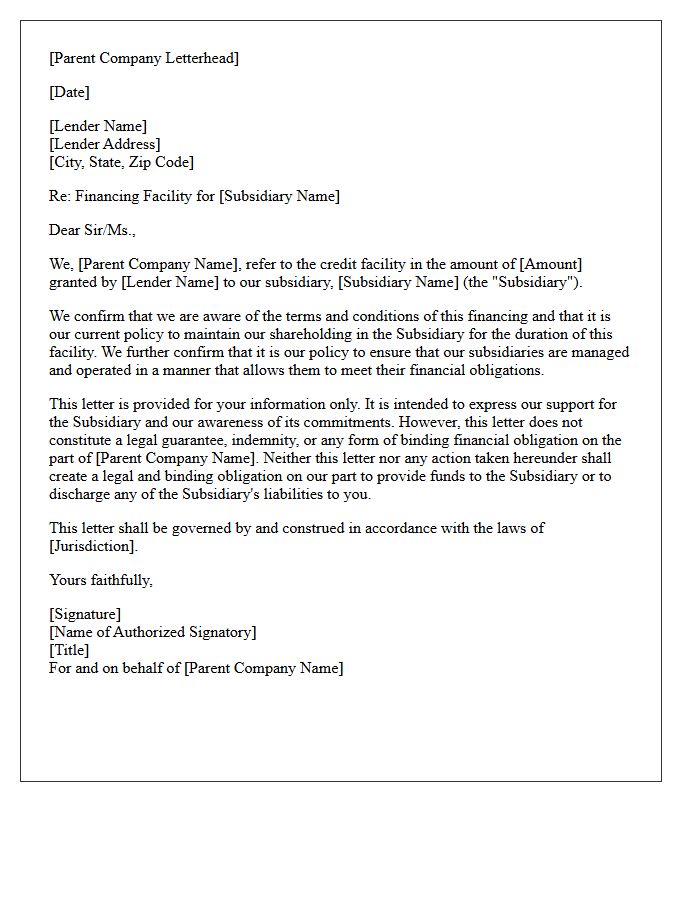

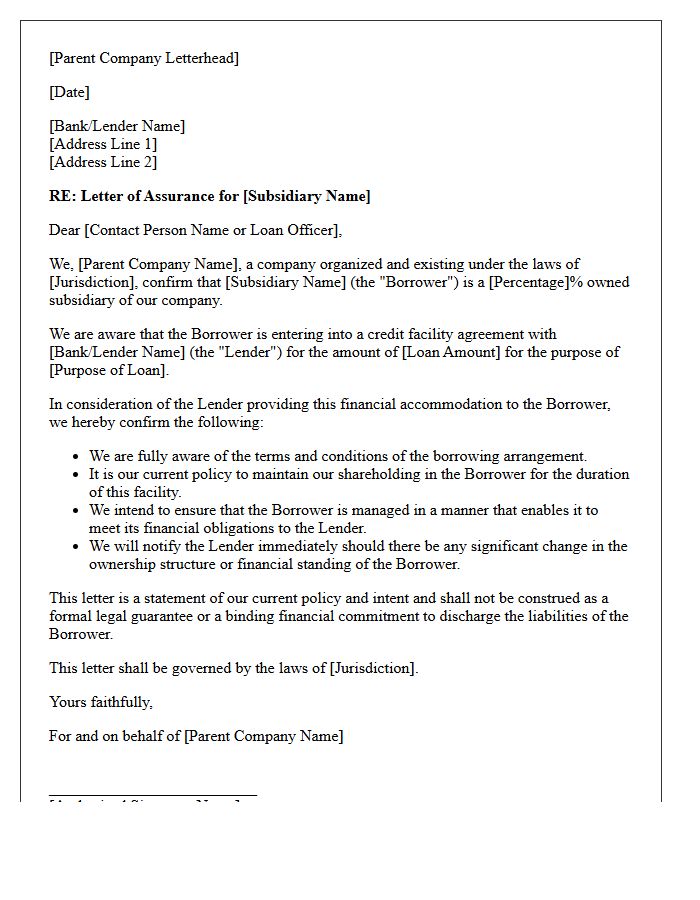

Parent Company Comfort Letter for Subsidiary Credit Facility

A parent company comfort letter is a document issued to a lender to support a subsidiary's credit facility. Unlike a formal guarantee, it typically expresses an intention to maintain ownership and ensure the subsidiary remains financially viable. While often considered a moral rather than a legally binding obligation, it provides essential reassurance to banks regarding the parent's commitment. Lenders use these letters to mitigate risk when the subsidiary lacks sufficient collateral or credit history, bridging the gap between a non-binding statement and a full corporate guarantee.

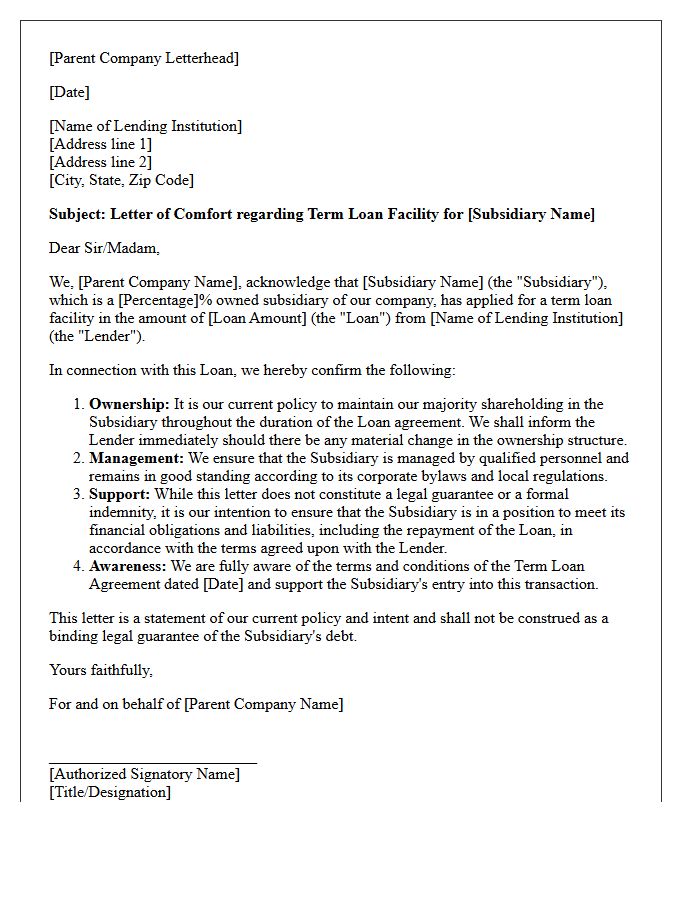

Letter of Comfort for Subsidiary Term Loan Agreement

A Letter of Comfort is a support document issued by a parent company to a lender regarding a subsidiary's term loan. While often not a binding legal guarantee, it serves as a moral obligation to ensure the subsidiary remains financially viable to meet debt commitments. Lenders utilize these letters to gain credit enhancement and reassurance of parental oversight. It is crucial to understand that the specific wording determines whether the commitment is merely a statement of intent or a legally enforceable obligation to provide financial support during the loan tenure.

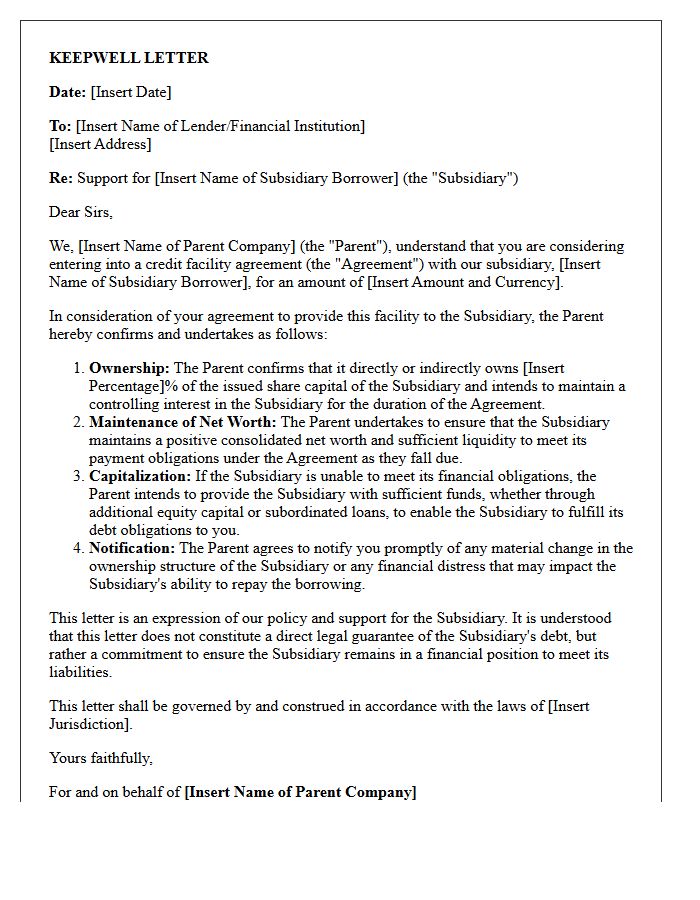

Standard Keepwell Letter for Subsidiary Borrowing

A Standard Keepwell Letter is a credit enhancement agreement where a parent company ensures its subsidiary remains solvent and maintains a minimum net worth to service debt. While not a direct guarantee, it provides comfort to lenders by promising financial support. It is a crucial instrument in international financing, often used when legal restrictions prevent formal guarantees. Investors must recognize that keepwell letters are generally moral obligations rather than legally binding payment contracts, meaning their enforceability depends heavily on specific jurisdictions and precise contractual language within the borrowing agreement.

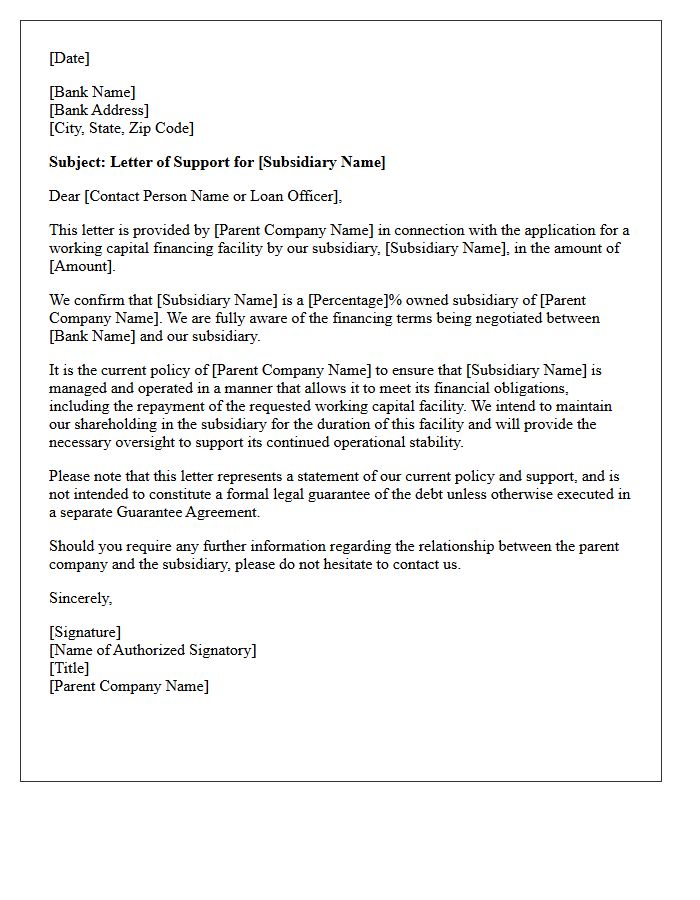

Letter of Support for Subsidiary Working Capital Financing

A Letter of Support is a critical document issued by a parent company to guarantee the financial stability of its subsidiary. It provides assurance to lenders that the parent will maintain the subsidiary's working capital and operational liquidity. While often considered a moral obligation, its wording can create legally binding commitments to cover short-term debts. This document is essential for subsidiaries with limited credit history to secure favorable financing terms and ensure continuous business operations by mitigating default risks for financial institutions.

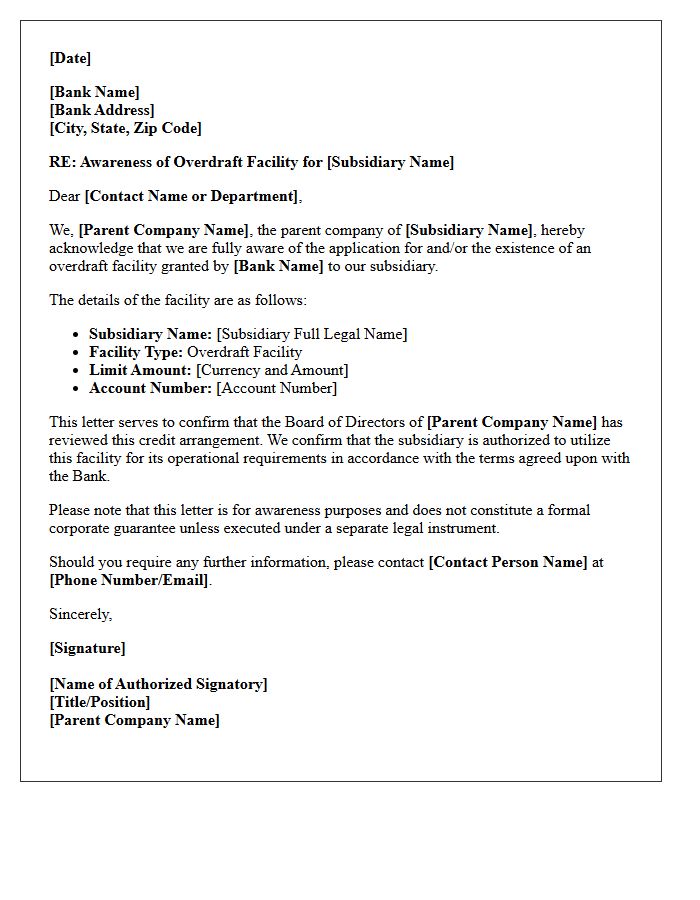

Parent Company Awareness Letter for Subsidiary Overdraft Facility

A parent company awareness letter is a comfort letter issued to a lender acknowledging a subsidiary's overdraft facility. Unlike a formal guarantee, it confirms the parent is aware of the debt and intends to maintain its equity stake in the subsidiary. This document supports credit approval by providing reassurance of the parent's ongoing support without creating a legally binding financial obligation. It is a critical tool in corporate financing that improves borrowing terms while managing the parent company's balance sheet liabilities and maintaining clear structural separation between entities.

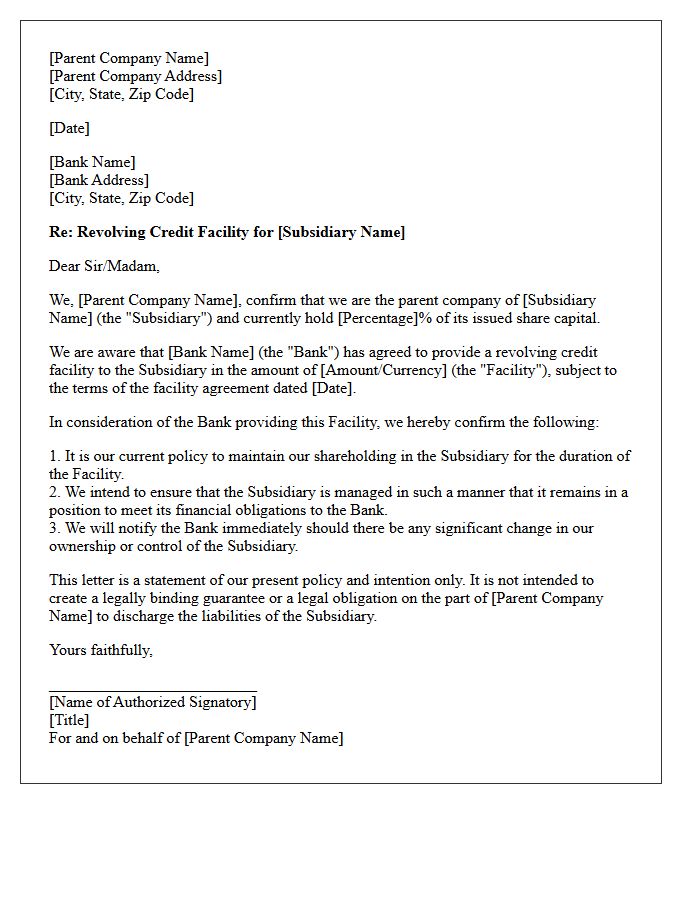

Letter of Comfort for Subsidiary Revolving Credit Line

A Letter of Comfort is a non-binding document issued by a parent company to support a subsidiary's revolving credit line. While it demonstrates intent to ensure the affiliate remains solvent, it typically lacks the legal enforceability of a formal guarantee. Lenders use it to assess the parent's commitment to the subsidiary's financial obligations. Businesses must carefully draft these letters to manage contingent liabilities while providing enough assurance to secure flexible funding. Understanding the distinction between moral support and legal indemnity is crucial for risk management and credit approval.

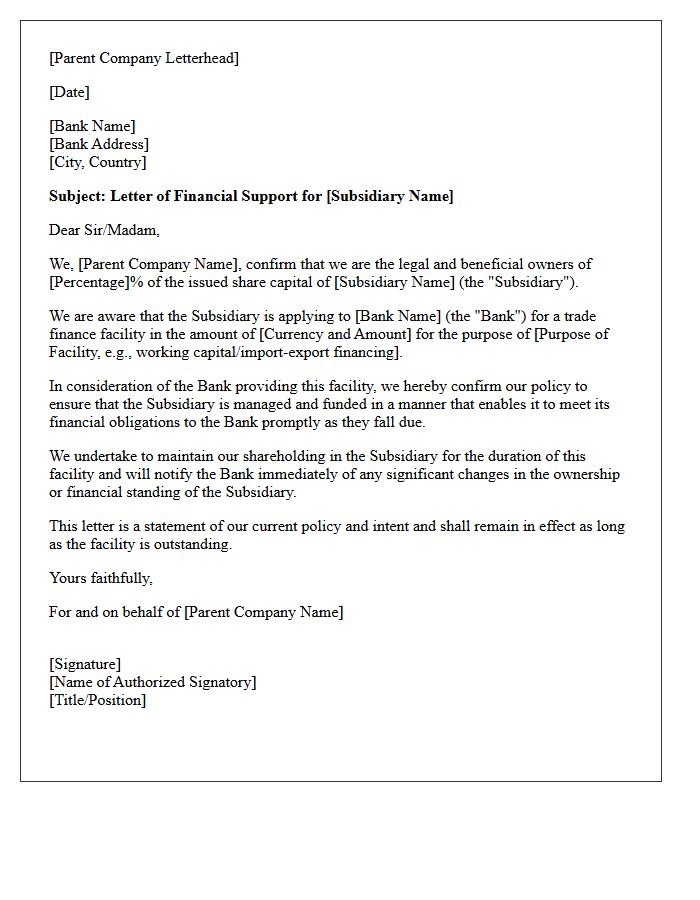

Financial Support Letter for Subsidiary Trade Finance Facility

A financial support letter, or comfort letter, is a formal document issued by a parent company to guarantee the creditworthiness of its subsidiary. In trade finance, this instrument reassures lenders that the parent will provide necessary liquidity to meet obligations. While often considered a moral commitment rather than a legal guarantee, it is essential for securing favorable credit limits and lower interest rates. Banks analyze these letters to mitigate default risk, ensuring the subsidiary maintains sufficient working capital to facilitate international trade transactions effectively.

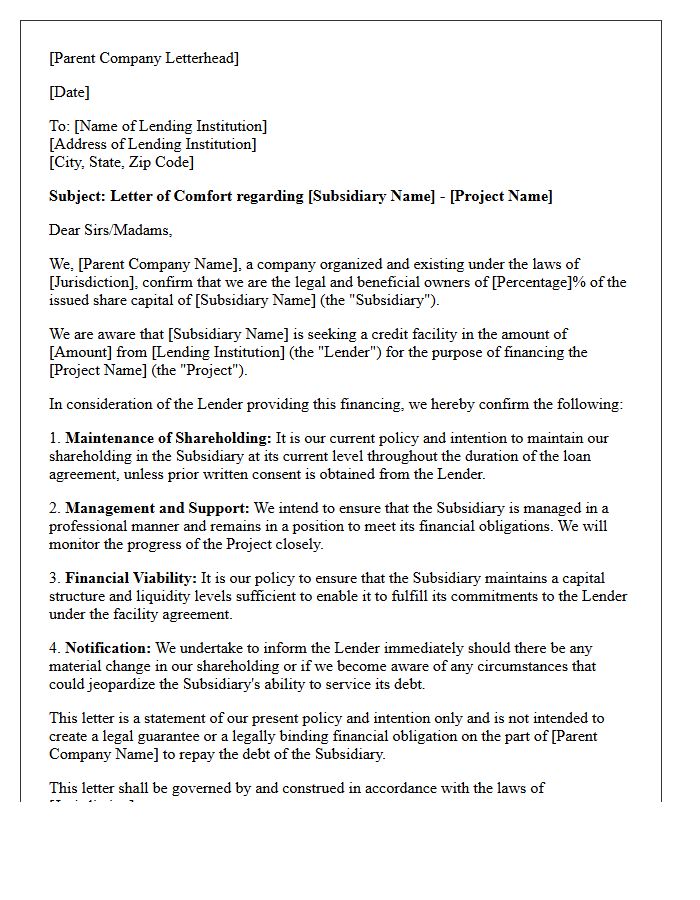

Parent Company Comfort Letter for Subsidiary Project Financing

A parent company comfort letter is a support document provided to lenders in subsidiary project financing. While typically non-binding, it expresses the parent's awareness of the debt and commitment to the subsidiary's success. It serves as a moral obligation to maintain shareholder control and operational oversight. Banks use these letters to mitigate risk when a formal corporate guarantee is unavailable. However, the specific legal enforceability depends on the precise wording, making it crucial to distinguish between a letter of intent and a rigorous financial indemnity.

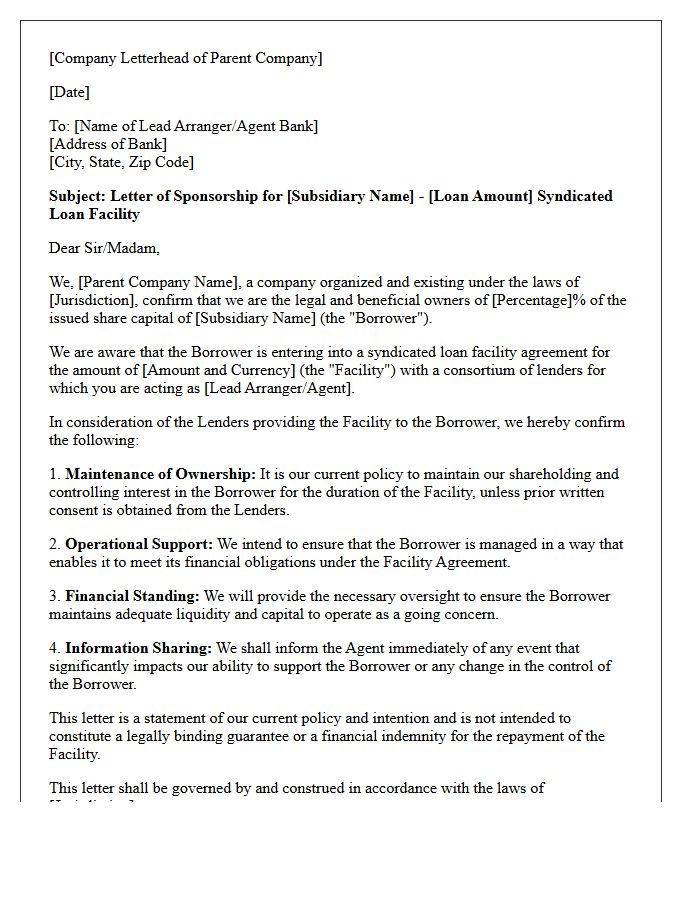

Letter of Sponsorship for Subsidiary Syndicated Loan Facility

A Letter of Sponsorship is a critical support document where a parent company provides assurance to lenders regarding a subsidiary's syndicated loan facility. It functions as a formal commitment to ensure the subsidiary maintains adequate liquidity and financial stability throughout the debt tenure. While often less binding than a full corporate guarantee, it enhances the creditworthiness of the borrower. Lenders rely on this instrument to mitigate default risks, ensuring the parent entity oversees the subsidiary's repayment obligations and operational continuity within the credit agreement.

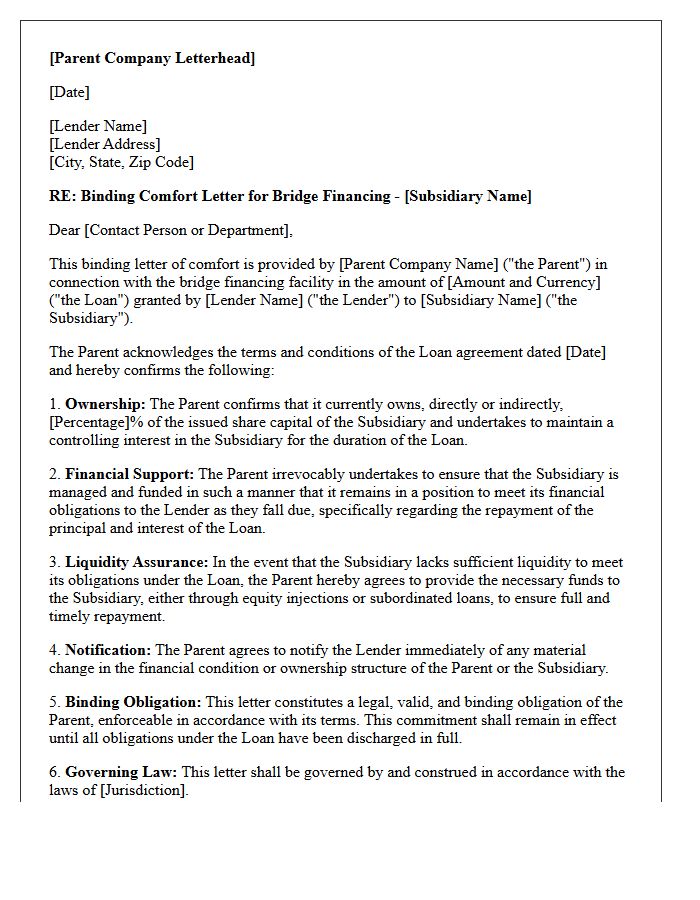

Binding Comfort Letter for Subsidiary Bridge Financing

A Binding Comfort Letter serves as a legal guarantee where a parent company ensures the financial obligations of its subsidiary. In subsidiary bridge financing, this document provides essential security to lenders during transition periods. Unlike non-binding versions, a binding commitment creates a legally enforceable obligation for the parent firm to maintain the subsidiary's liquidity and solvency. This structural support reduces credit risk, facilitates immediate capital flow, and guarantees that short-term debts are satisfied if the subsidiary faces cash flow constraints before securing permanent long-term funding.

Non-Binding Comfort Letter for Subsidiary Debt Obligation

A non-binding comfort letter is a support document issued by a parent company to reassure lenders regarding a subsidiary debt obligation. While it conveys intent to maintain the subsidiary's financial health, it lacks legal enforceability compared to a formal guarantee. Investors should recognize that these letters represent a moral commitment rather than a contractual liability. They are primarily used to improve credit standing without adding debt to the parent's balance sheet. Understanding the distinction between a "soft" and "hard" comfort letter is vital for assessing true credit risk exposure.

Parent Company Letter of Assurance for Subsidiary Corporate Borrowing

A Parent Company Letter of Assurance, often called a Keepwell Agreement, is a formal commitment issued to lenders to support a subsidiary's financial obligations. While not a direct guarantee, it enhances the subsidiary's creditworthiness by ensuring the parent maintains the entity's solvency and liquidity. This document provides reassurance to creditors that the parent will oversee operations and provide necessary capital. It is a critical instrument in corporate finance to secure favorable borrowing terms without officially recording the debt as a contingent liability on the parent's primary balance sheet.

What is a parent company comfort letter in the context of subsidiary borrowing?

A parent company comfort letter is a document issued to a lender expressing the parent's awareness of and support for a subsidiary's loan. While it outlines the parent's intent to ensure the subsidiary remains solvent and meets its obligations, it is generally considered a statement of intent rather than a legally binding financial guarantee.

Is a comfort letter legally binding for the parent company?

In most jurisdictions, a comfort letter is categorized as a moral obligation rather than a legal contract. Unlike a formal guarantee, it does not typically grant the lender a direct legal claim against the parent's assets, though the specific wording can sometimes lead to legal liability if it contains actionable representations.

Why do lenders accept comfort letters instead of formal guarantees?

Lenders may accept comfort letters when a subsidiary has a strong credit profile or when the parent company is prohibited from providing formal guarantees due to restrictive covenants, regulatory limits, or internal policy. It serves as an assurance of the parent's ongoing commitment to the subsidiary's operational stability.

What are the typical components of a comfort letter for subsidiary financing?

A standard comfort letter usually includes a confirmation of the parent's shareholding percentage, an acknowledgment of the specific loan facility, a statement of policy regarding the subsidiary's financial maintenance, and an undertaking to notify the lender of any significant changes in ownership.

How does a comfort letter affect a parent company's balance sheet?

Unlike a financial guarantee, a comfort letter is generally treated as a contingent liability and does not typically require a line item on the parent company's balance sheet. However, depending on the strength of the language and accounting standards (such as IFRS or GAAP), it may require disclosure in the footnotes of the financial statements.

Comments